Benchmarking a Great Supplements Brand

What makes these brands cash printers

Why historically do investors like software companies so much?

Well - because investors are lazy and greedy pigs; and software [was] the perfect model for a lazy greedy pig - high margin, sticky, scalable, all the good stuff.

The reason high margin sticky scalable products are so desirable is because when you put that all together and you get…….profits! sweet sweet profits

Supplements are the closest category in CPG that can look a bit like a SaaS model.

They’re high margin, can be extremely sticky, and very scalable.

As many of you know, my company iris works with lots of CPG brands. Our largest segments are beauty and supplements - followed by apparel food and beverage, with just a touch. Iris has around $30B of GMV in its databases; and its not a stretch to say that we have more visibility into what drives profits at brands than anyone else in the entire CPG industry. About a fourth of that is supplements revenue.

So, I thought I’d bless you all with some data and insights.

Let’s get into it

We typically like to do the benchmarking on a variety of things:

LTV:CAC components

nAOV, rAOV, retention rates, gross margin, CAC

MER

Opex

LTV:CAC benchmarks

A few years ago the industry woke up to contribution margin. This was because financial savviness was required to stay alive post the free money era.

Now - post gruns exit - it feels like the industry is waking up to LTV:CAC. What’s ironic about that is that LTV:CAC is contribution margin, in many ways. Let me explain.

LTV = Revenue - COGS

CAC = marketing

Revenue

LESS: COGS

EQUALS: Gross Profit

LESS: Marketing

EQUALS: contribution margin :)

So you can literally feel the industry maturing and getting more sophisticated.

Anyways I digress.

I am going to provide the thresholds to be top decile for each benchmark. If you want more you can come check out iris at irisfinance.co - or just email me, u can reply to this.

Benchmarks:

AOV

Top decile AOV: $80

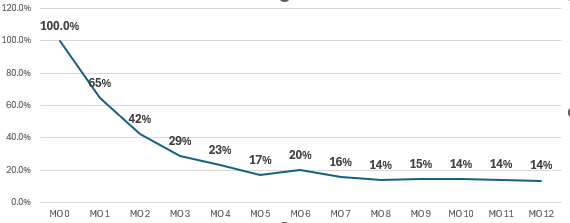

Retention Rates

Top decile dollar based retention rates on ALL customers. So many of you chuds like to only look at subscribers. To be fair look at both but this is for ALL. if your mo12 DBNR is 12% or higher you are in elite territory

Gross Margin

Top Decile GM: 65.95%

MER

Top Decile MER: 5.07x

opex

Top Decile opex as a % of revenue: 8%

So if we put that altogether, a top decile supplement brand is selling for $80, getting about 3.8 purchases per year ($304 12mo LTR) at a 65% margin ($197 12mo LTV); fantastic unit economics.

Meanwhile the P&L looks something like a 65% gross margin, 20% on marketing for 35% contribution, with 8% opex meaning 27% EBITDA margins.

In reality, almost no one has all of these attributes, and EBITDA margins even for the strongest of brands are lower than that - but if you were to build the perfect supplements brand, that’s what youd be shooting for.

The order of operations

The other thing to consider as an operator is how to prioritize your efforts in improving all of these benchmarks. It may sound hard, but its actually extremely easy; all you need to do is pick the benchmarks with the highest increase in enterprise value should you achieve top decile in that benchmark.

So if you see an opportunity to increase EBITDA 500k on one benchmark, and your business is worth 8x, thats a 4m tickup in EV.

This excercise also helps you figure out what you should not spend time on. For example, if you are already world class at retention, but gross margin sucks - dont spend all your time and money trying to get better retention.

It’s all about building your business with visbility into the things that you can and should make better, and not spinning wheels on the things that are already working or outside of your control.

Namaste friends