Only Fans Financial Breakdown

Only Fans Financial Breakdown

There’s nothing more capitalist than making a billion dollars off of nudity.

Despite the fact that this is actually some of my best work- I am a little late on this admittedly. Having a newsletter is actually a decent amount of work. Anyways, Only Fans filed financials the other week and MAN WAS IT JUICY.

Here is the link to the materials

let’s start off with a nice sankey diagram (I made this) and of course, the P&L:

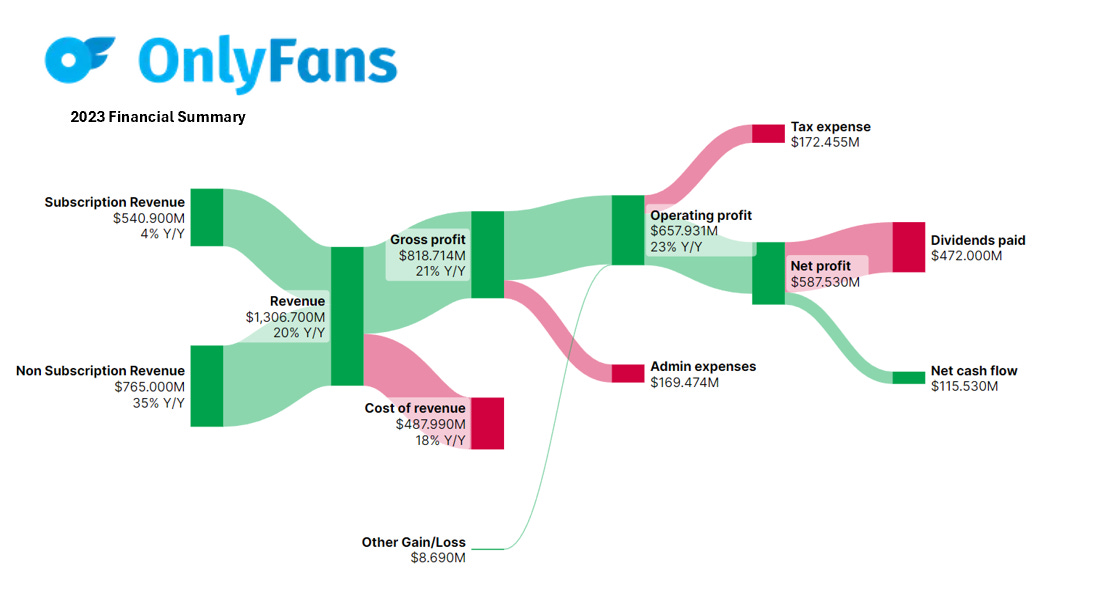

The story was really that the owner of OnlyFans has paid himself over $1.1 BILLION dollars in dividends since 2019 (more on that at the end)

What kind of business can do that? A hyper profitable one of course. Only Fans is the marketplace business model earnings power on full display. Boasting operating cash flow yields in excess of 50 (read: FIFTY) percent, Only Fans is a cash printing machine with hardly any comparables.

First, a brief history of Only fans

Only fans was started in 2016 by British entrepreneur Tim Stokely that allows creators to monetize their work directly with their fans. Initially the traction was in fitness trainers, chefs, and musicians. However, quickly after the 2016 launch the site became a hotbed for ‘adult content’ (read: porn). In 2018, Lenonid Radvinsky bought a controlling stake in the company, which has been… a decent investment.

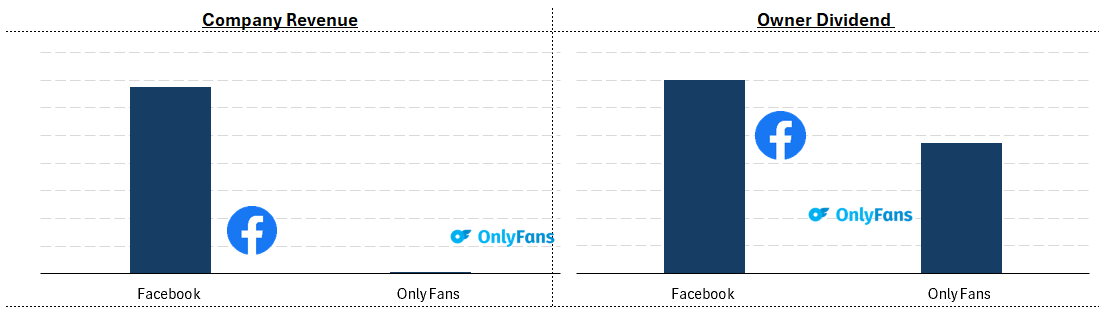

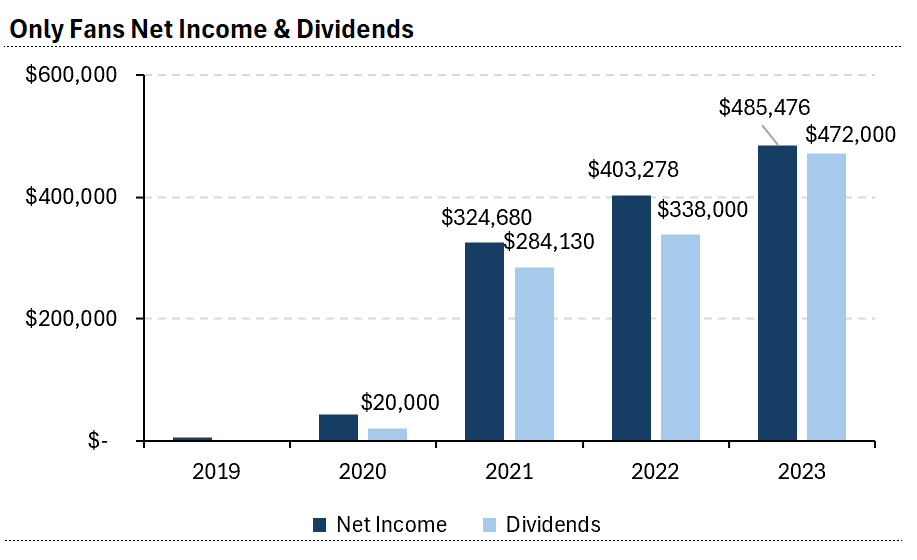

Radvinsky has paid himself over $1B in cumulative dividends since acquiring the business in 2018

Most recently, Radvinsky pocketed an eye watering $472MM paycheck in 2023, up from his not so bad $338M the year before. For context, Mark Zuckerberg makes about $700m of dividends per year from his facebook holdings. Yes I realize Facebook has a way bigger market cap and is public and has shareholders, thats not my point I’m just giving context:

But really - how is this even possible? This is crazy crazy earnings. What makes Only Fans so profitable?

Let’s dive into the business.

Most simply put - this is a marketplace model at its best. Only fans has solved one of the hardest problems in business, that is only associated with the market place model - the chicken and egg (read: supply and demand) problem. When you solve this problem as a market place model you are rewarded handsomely. Marketplace business models like Amazon and Airbnb to name 2.

BUT, Only Fans actually goes one step further - they have managed to monetize their marketplace via subscription. Amazon prime is another marketplace with a subscription model, and thats a big part of why Amazon has become Amazon. Airbnb, for example, is a more traditional take rate model.

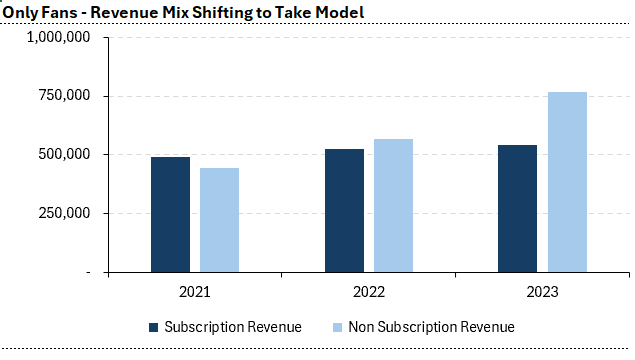

Only Fans revenue historically has been about 50% take and 50% subscription, as pictured below:

However, as you can see - this revenue mix is obviously shifting towards non subscription; read: take rate.

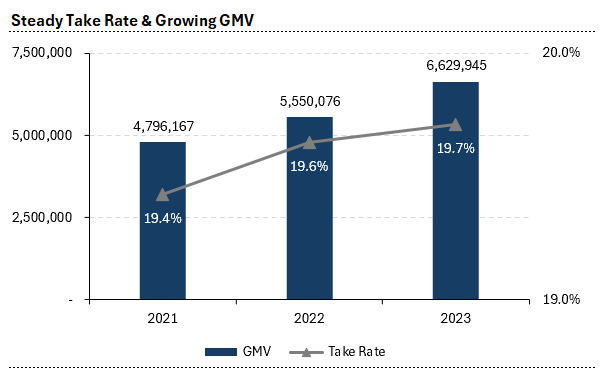

Amazon famously has a massive take rate of around 35% - meaning every dollar that gets sold by an Amazon seller, Bezos & Co are collecting 35 cents - thanks for playing.

Only Fans has recently been able to massively grow their non subscription revenue by keeping the take rate intact and driving GMV growth. Slight take rate expansion from 19.6% to 19.7% helped drive a faster YoY revenue growth than GMV growth by about 50 basis points, also driving about 90 basis points of operating margin expansion YoY from ~49% to 50%.

As a marketplace, it is all about the supply side for Only Fans. A sort of ‘build it and they will come’ approach to sex (basically). In 2023, creator growth was faster than fan growth at 29% and 28% respectively. Only fans continues to grow its GMV in large part thanks to its brand which has aggregated much of the demand side.

GMV per fan and per creator both peaked in COVID, unsurprisingly.

The cash flow.

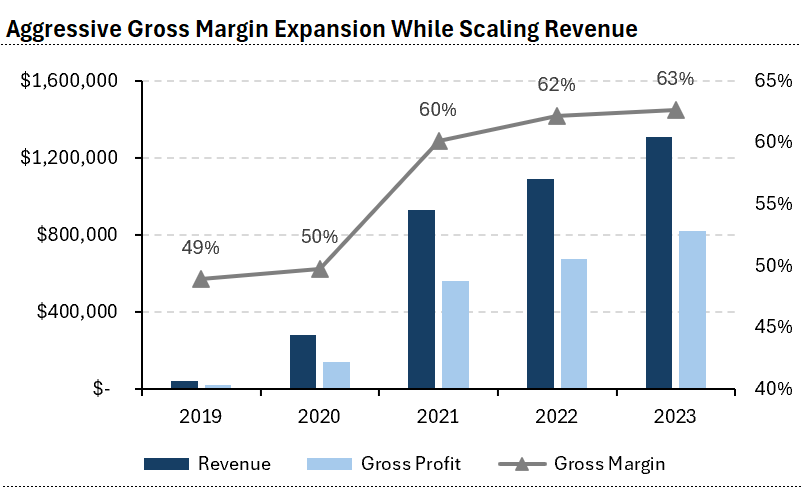

What is so mind boggling about OF is not that its cracked the marketplace model, but that its spitting off such ridiculous cash. In 2020, the operating cash flow yield was SEVENTY PERCENT. That is legitimately a world class GROSS MARGIN for any other business.

OF pays a decent amount out to its creators as a ‘cost of sale’ - which is overwhelmingly their largest expense.

The company has seen its ability to hold onto some of those commission dollars increase during COVID - with gross margin increasing from 50% in 2020 to 63% in 2023.

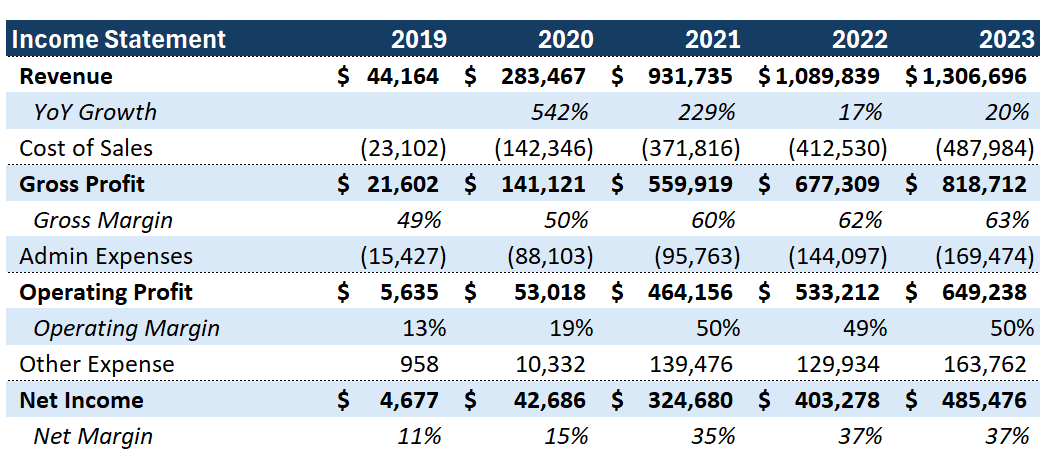

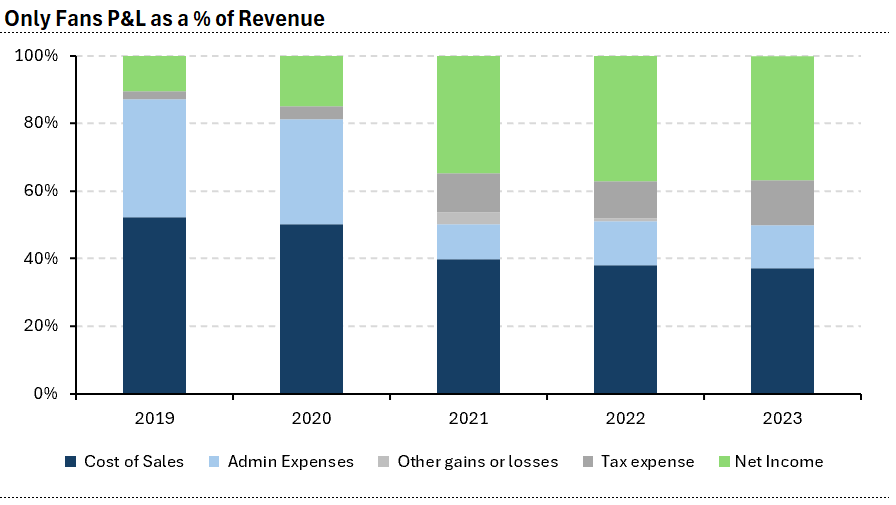

What’s more important, and impressive, is that operating margin expanded thirty (THIRTY) full points during this time. Just over 10 points from gross margin expansion, and 20 from operating expense leverage:

When we chart the P&L lines as a percentage of revenue, the most noticeable is the light blue shrinking rapidly while revenue grows:

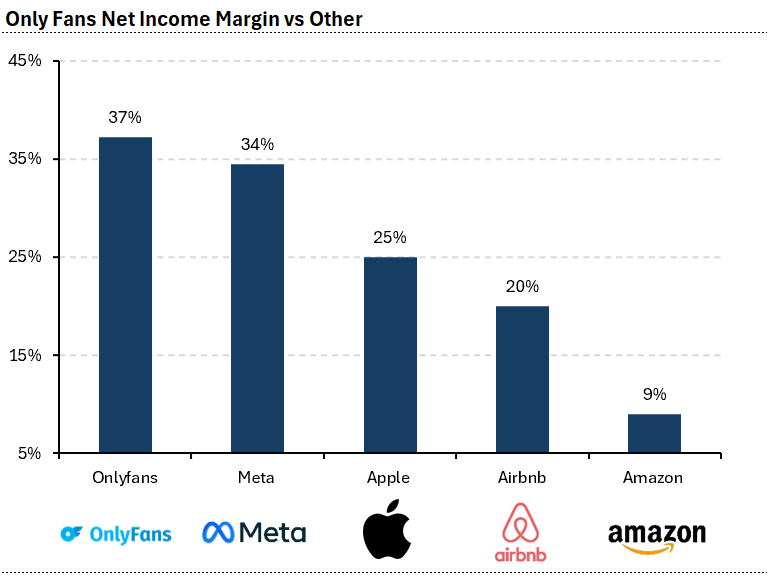

All of this is what causes OF to deliver some of the highest profit margins of any business, netting over 37% of revenue in 2023 in net income - this is higher than Amazon, Apple, Meta, Airbnb - and almost any other company I could think of with the exception of Nvidia:

This earnings power is what makes the owner of the company very, very rich. As he has not been shy to pay out his share of the profits. In 2023, the declared dividend was 97% of net income, bringing OF’s total net cash flow down to just over $100mm.

This dividend, as far as I can tell, is easily a top 10 payout for a private company and maybe top 5. Here are a few other dividends for context:

Cargill - $1.13B in 2022

Mars - Est. $500m-1B

Publix - Est $5-600m

Radvinsky owns a couple other porn sites like “MyFreeCams’ - so this guy definitely has no problem with making money this way.

All in all, Radvinsky has kept a pretty low profile despite having to file this information in the UK. There is no specific public record of extravagant personal purchases like luxury homes, cars, or other high-profile assets commonly associated with tech entrepreneurs or wealthy individuals. Details about his lifestyle, such as hobbies, preferences, or social activities, are not well-documented in public sources. Radvinsky appears to prioritize keeping his personal life separate from his business activities.

Im speculating here, but it does seem like he kicked out the original founders as soon as things started getting really profitable.