Prestige Consumer's $1B Acquisition of Breathe Right - the deal no ones talking about

& why you should care - a deep dive into the transaction

This week, Prestige Consumer Healthcare (NYSE: PBH) - a $2b mkt cap rollup of OTC brands including Dramamine, Clear Eyes, and more - closed its $1.045B acquisition of nasal strip brand Breathe Right.

The reason I want to go deep into this transaction is because it represents a relatively ‘cookie cutter’ deal. Its not one of these high flying VC backed emerging brands that we’ve seen so many of over the last few years. We can learn alot about M&A by diving into a more ‘boring’ Breathe Right transaction, which will make you smarter than everyone else who didn’t want to take the time to understand it bc it wasnt gruns.

Let’s get into it

A bit of history on Breathe Right

ok quick primer. Breathe Right was commercialized out of a company called CNS Inc out of Minnesota neurology equipment business in 1990.

Nose strips were actually one of the OG athlete endorsement playbooks after it became really popular for football players to wear them

by 2006 CNS boomed to over $100m in sales, or $160m in todays dollars, and was ultimately acquired by GSK (big pharma co) for $566m (4.8x sales).

Fast fwd to 2020, and Foundation Consumer Brands (a platform backed by PE), acquired Breathe Right, Dimetapp, and 5 other brands in a corporate carveout - while the acquisition price was undisclosed; Foundation was a $261m vehicle, so i might roll with that as the entry price in 2020.

Foundation is who sold the property to Prestige Consumer Healthcare (NYSE: PBH) - the owner of brands like for $1B+ this week; here’s their portfolio. All of them are #1 or #2 in a small, durable, low-attention category that a P&G or a Haleon would never bother to optimize.

The model is straightforward and it’s closer to LBO mechanics than to strategic M&A:

Acquire mature, category-leading OTC brands that are non-core somewhere bigger.

Run them asset-light; outsourced manufacturing, lean overhead, disciplined A&P.

Harvest the free cash flow.

Use the FCF to de-lever.

Repeat.

Their organic growth algorithm is a deliberately modest 2–3%. They are not trying to reinvent these brands. They’re trying to own predictable cash flows and compound via M&A. That makes them the natural terminal buyer for a brand like Breathe Right , and puts them in the same competitive set as Church & Dwight’s tuck-in machine, Helen of Troy, Central Garden & Pet, and Spectrum Brands.

The wrinkle: this was a stretch for them. At announcement Prestige carried a market cap around $2.84B, so a $1.045B deal is ~37% of the company its largest acquisition ever, after years spent deliberately deleveraging and growing organically. This is Prestige stepping back into aggressive M&A in a real way.

The Deal

Headlines:

Enterprise Value: $1.045B

EV net of tax benefits: $900m

EV/rev: 5.2x

EV/EBITDA: 11x / 9.5x net of tax

sell side: Cannaccord

buy side: Citi

Breathe Right itself is ~two-thirds of the portfolio's revenue and profit; Dimetapp and Anbesol carry most of the rest.

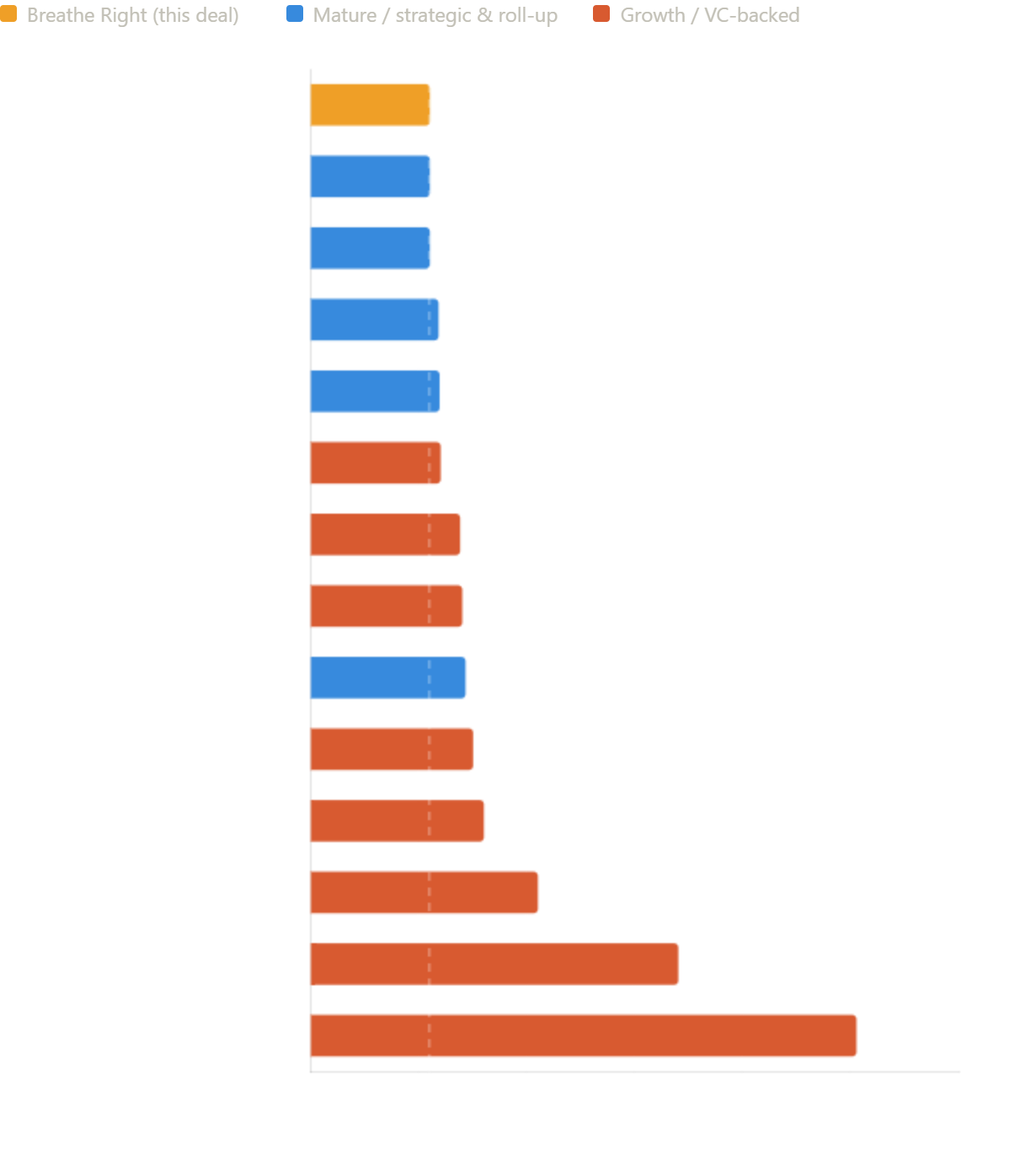

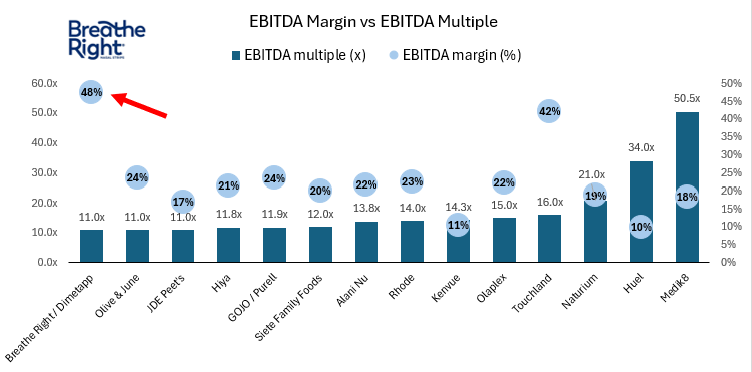

Here’s the comp set on EBITDA:

A couple things stand out:

1 - 11x EBITDA / 9.5x net of tax is at the very low end of the comp set

AND THEIR EBITDA MARGINS ALMOST 50%

2 - 5.2x sales multiple is a borderline irrelevant here

it’s just an exemplification of how profitbale this company is. 5.2x sales is extremely rich, while 11x ebitda is very average.

Structure

The deal was structured as an asset purchase; not a stock purchase - this is the driver of the ‘net of tax’ $900m EV and consequential exit multiples.

In an asset deal, the buyer takes a stepped-up tax basis in the acquired intangibles; the brand, the goodwill, the ‘customer relationships’ and amortizes that step-up over 15 years.

Those amortization deductions decrease income and generate real cash tax savings. Its like how interest is tax deductible.

Discount that stream of savings back to today and you get the ~$150M present value Prestige is citing. Net it against the $1.045B sticker and the economic purchase price is ~$900M, which compresses the effective entry multiple from 11.0x to ~9.5x EBITDA.

Financing

This section is for the dawgs. buckle up.

Prestige funded the deal with cash on hand plus a new Term Loan B. i.e., they levered up. You can only do that when the underlying cash flows are predictable enough to service debt, which is precisely the quality a 30-year-old #1 brand has and a viral two-year-old DTC darling does not

Thats wht makes this transaction look alot like an LBO despite the fact that its being done by a public strategic.

Prior to the deal Prestige didnt have much debt, about 2.6x leverage (net debt/EBITDA) - under the 3.0x target they are comfortable with. They even bought back $156m of stock recently.

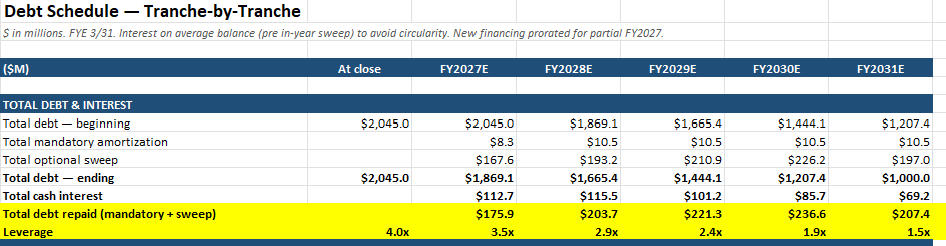

The Breathe Right acquisition was funded almost entirely with new debt. They took out a $1.045B term loan, basically one big loan from a syndicate of institutional lenders to cover the whole purchase price, with the option to borrow another $95M later for a smaller deal. They also bumped up their backup credit line to $225M and pushed its due date out five years. A little cash covered the fees.

So if they were at 2.6x leverage with $$346m in EBITDA / $900m net debt - another billion basically doubles that leverage ratio to 4.0x; thats redlining a bit

This is where those sweet sweet ebitda margins come in from breathe right

They can delever back down to sub 3.0x in just 2 years by growing revenue just 2% per year, growing combined EBITDA to $463.5m by 2028 and paying down just under $400m in the debt to delever to 2.9x.

The takeaway

In a world of sexy VC backed growth exits; a good old fashioned cash flower can support large valuations - despite only growing 2-3% last year, Breathe Right earned a billion dollar price tag because the buyer could fund the whole purchase with debt and credibly underwrite a path towards paying down those borrowings.