UNDERWRITING LIQUID DEATH

WHAT's REALLY GOING ON + NEW INFO

This week is was reported by our friends at The Information that Liquid Death was set to raise a $20m round to ~fuel growth~. I thought this was a pretty odd number to report considering the last fundraise was 9 figures.

Is this a desperate bridge round, or a real financing to fuel growth? There have been mixed reports of what is going down at one of the decades buzziest beverage brands - but fear not, I am here to shed light.

Let’s underwrite liquid death

OK, so what do we know? A few things:

$340m 2025E revenue (+40% YoY)

$240m 2024A revenue (reported by company)

$~400m raised, latest valuation $1.4B

Founded in 2019

Huge TAM

Founder is definitely really rich (matters, imo)

Existing investors include: Science, Riverside Ventures, Groundforce capital, Steve Aoki, and a whole lot more.

So liquid death’s fundraising history looks like this:

Revenue

$340m in 6 years is nothing to sneeze at. This is real growth in a real category - but this company has raised far too much money to get there and is still on the wrong side of revenue to dollars raised.

But alas my friends - this is the past! We’re not underwriting the past, we’re underwriting the future!

LD is allegedly going to grow 40% this year - so if that growth rate dips to 30% in 2026, 25% in 2027, and 20% in 2028, the company will be around $663m in revenue:

My sources tell me that the burn for LD last year was $50m. Woof. Candidly that’s just a non starter and the company will sell for its pref if that doesn’t change - so if we’re investing in LD, we have to believe they can figure that out while maintaining growth - otherwise we’re a pass.

Entry Valuation

This round is almost certainly coming on a flat valuation of $1.4B from the last round, which is 4.12x this year’s sales - rich.

Exit Valuation

Ok - so let’s just imagine that Drew has achieved his childhood dream of becoming a VP level at a tier 2 or 3 growth equity shop and the liquid death deal hits his desk. We’ve already established what we have to believe to not immediately rip it up and throw it in the trash - so what do we have to believe as far as an exit?

Well - the good news is that this space is obviously SCORCHING with large M&A this year; and there’s no real reason to think that can’t continue or even accelerate with a few anticipated rate cuts toward the end of this year.

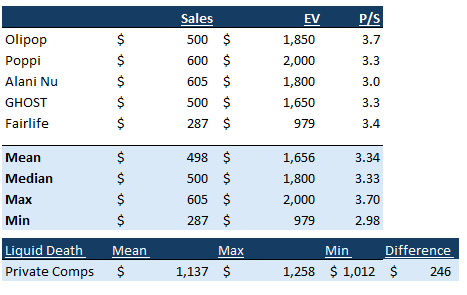

So let’s establish the comps:

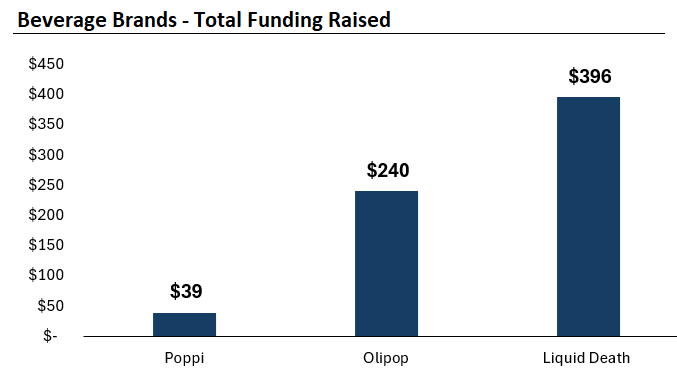

Olipop

Poppi

GHOST

Alani Nu

Fairlife

The sales multiples of this comp set are as follows: - Mean: 3.34x - Median: 3.33x - Min: 2.98x - Max: 3.70

So let’s throw together a quick sensitivity table to see where things start to get interesitng. I’m going to put revenue as one variable - where it can go both up and down; and then I’m also going to make exit multiple a variable based on this comp set:

Ok - so as you can see, really two things have to happen for me to even have this conversation:

Revenue passes ~$540m

Exit multiple is AT LEAST the median

Ok, revenue of $540m? Doesn’t seem unattainable by any means. BUT, there’s obviously a really good chance growth completely stops or slows meaningfully when we move to get burn in check. Need to understand the business model better and if there’s bloated opex, or if this revenue is propped up on excessive marketing.

Average exit multiple? Sure, I don’t see why if things go right LD would trade for any meaningful discount.

Ok so far I am not overly excited, but I’ll have the conversation. If its gonna take 4 years and EVERYTHING goes right and they get the most bottom right valuation in my sensitivity it would return 20% on an IRR basis, so I’m at the table, as the optimist that I am.

But honestly, I need this one to return more than 20%. More like 30%; its gotta be a higher return because I consider it to be higher risk given the current burn on the company.

30% IRR over the same hold period would be a $4b exit value.

What do you think? Can LD pull of a $4B exit?