Updated thoughts on IM8 ($PRE)

A deep dive into the cohort model

IM8 is no doubt one of the hottest brands in consumer right now. I was the first to start talking about the company - I’ve researched, modeled, and written extensively about the business. The CEO danny came on my podcast, I chat with some of their investors, and their new CFO is a local friend of mine here in chicago as well. I have followed this story closer than anyone and I have invested a significant amount of money into the company.

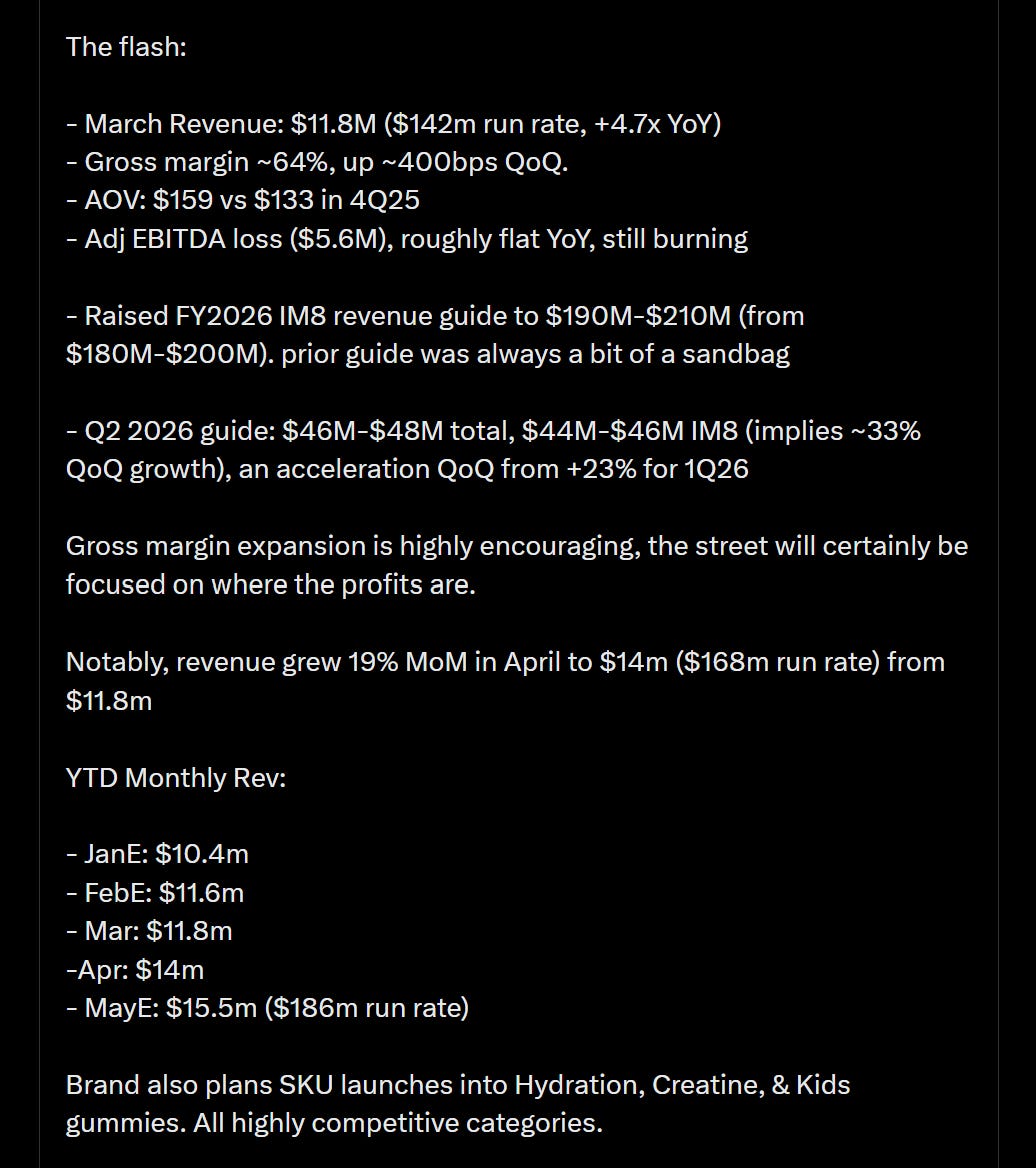

Yesterday they published a preliminary earnings report that gave us lots more data on the company. I dont know why they published this report, maybe they expected the stock to trade up on the continued revenue momentum (which is exceptional) but I am here to break down the report and provide you with an update on my latest thoughts on the company.

A flash look:

Let’s get into it

A brief primer on im8

Ok so if you dont know im8/prenetics you can get my initiation report here, or listen to my podcast with danny here.

I’m going to try to give you the short background. you will understand why i said try in a second.

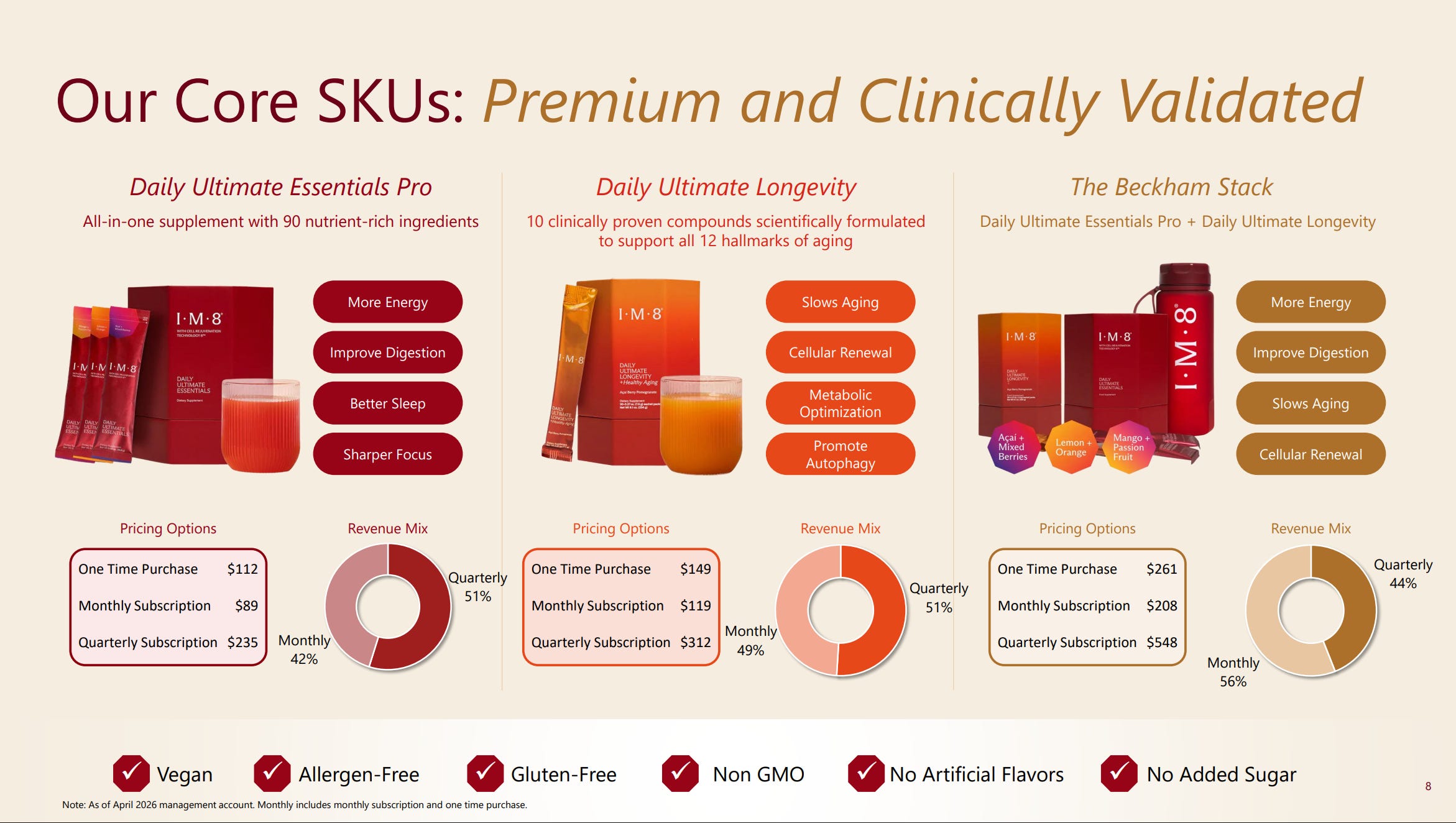

Prenetics is a chinese based company co founded by david beckham that SPACed as a diagnostics & bitcoin treasury company during covid that pivoted to selling supplements and subsequently launched the fastest growing supplement of all time, IM8 - a daily health product. I will also add I’ve been using im8 for probably 8 months or so now, and i do really like the product. It was a NEED when i was running a retatrutide cycle.

The report

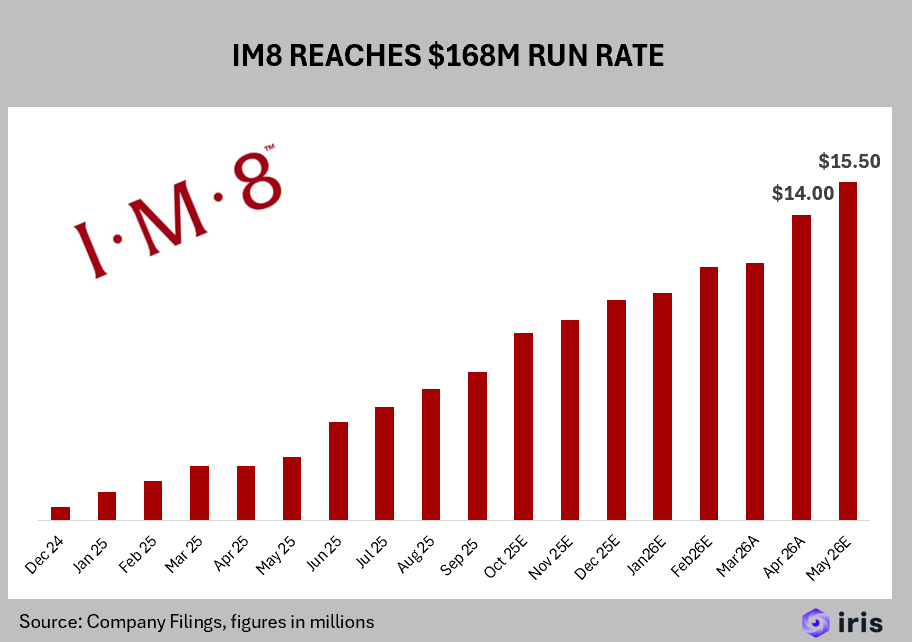

The headline here was accelerated revenue growth. IM8 hit $14m in sales in april (month 16), and management raised guidance from 180-200m to 190-210m. I expect they will raise guidance again or at least end up at the top of that range.

The last two earnings reports have been pretty much in line with expectations and so there haven’t been big moves in the stock.

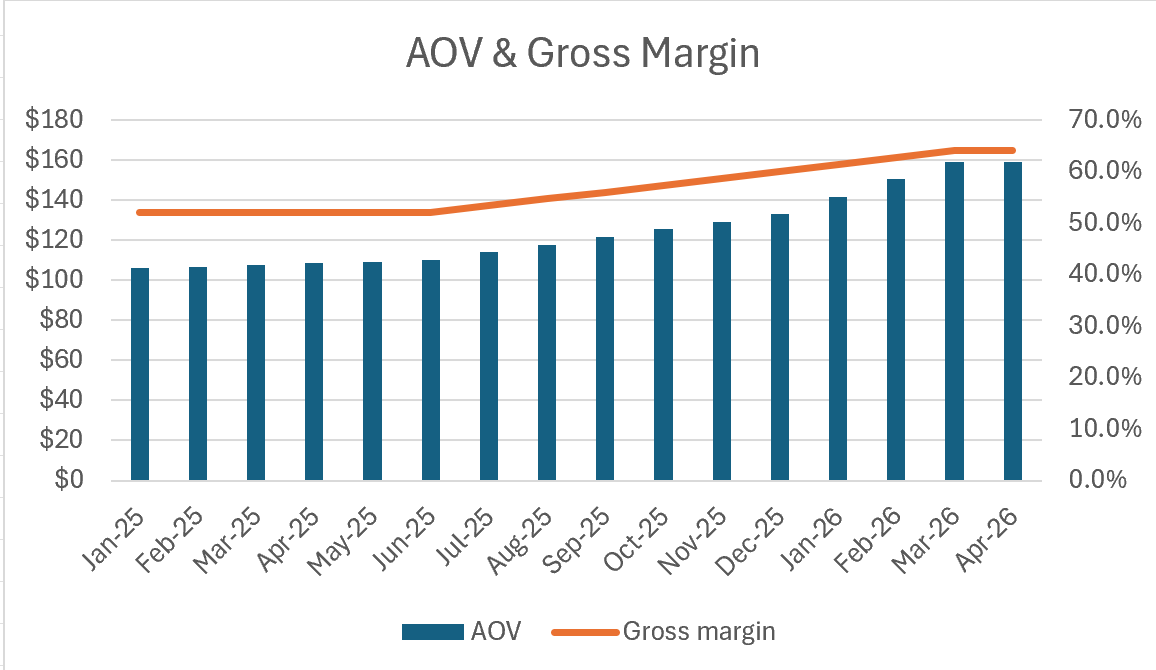

AOV continues to make huge moves up ($240 for new customers!!), as the company is pushing 90 day supply bundles and 90 day subscriptions. At the same time, gross margin expansion from 52% to 64% in short order is highly encouraging

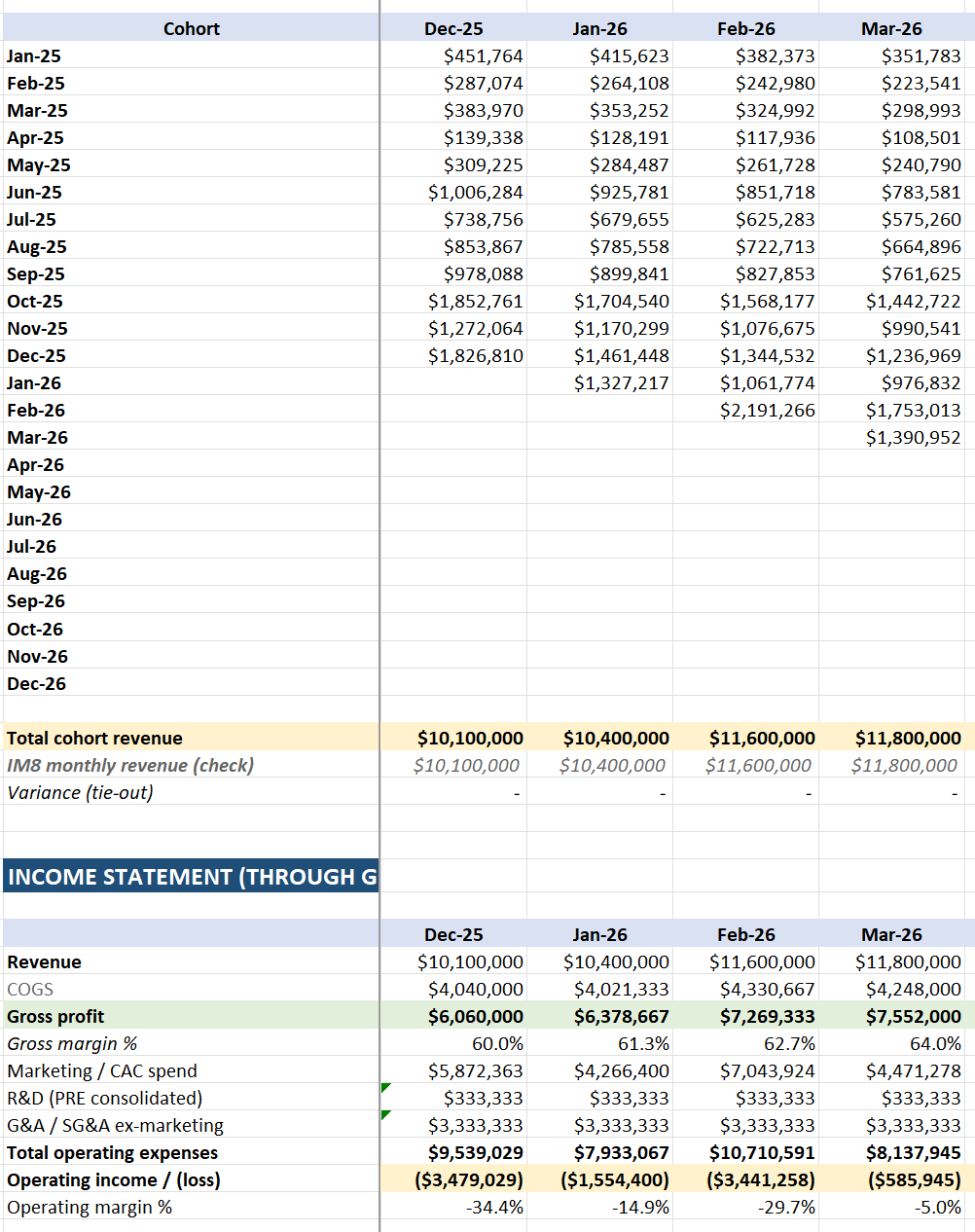

I’ve taken the liberty of vibemodeling with iris the cohort revenue model (this is something what we do all day every day at iris with our agents) in order to try to pin down whats going on here. The disclaimer is that we are operating on VERY limited information, including LTV and retention which IM8 has not reported on in a long time.

Ive reconstructed the revenue model, applied gross margins, and made some opex/marketing assumptions to get to the -5.6m adj ebitda figure below:

So we’ve come up with some guesses on marketing asusmptions, as well as cohort sizes based on revenue and AOVs. We have revenue numbers, and we’re given AOV and gross margin numbers as well as some CAC numbers in the past, so we’re able to reconstruct some of the cohort variables. The last reported CAC was $104. AOV has gone up a TON since then, so the implication is that cac has gone up even more since the company is still losing money.

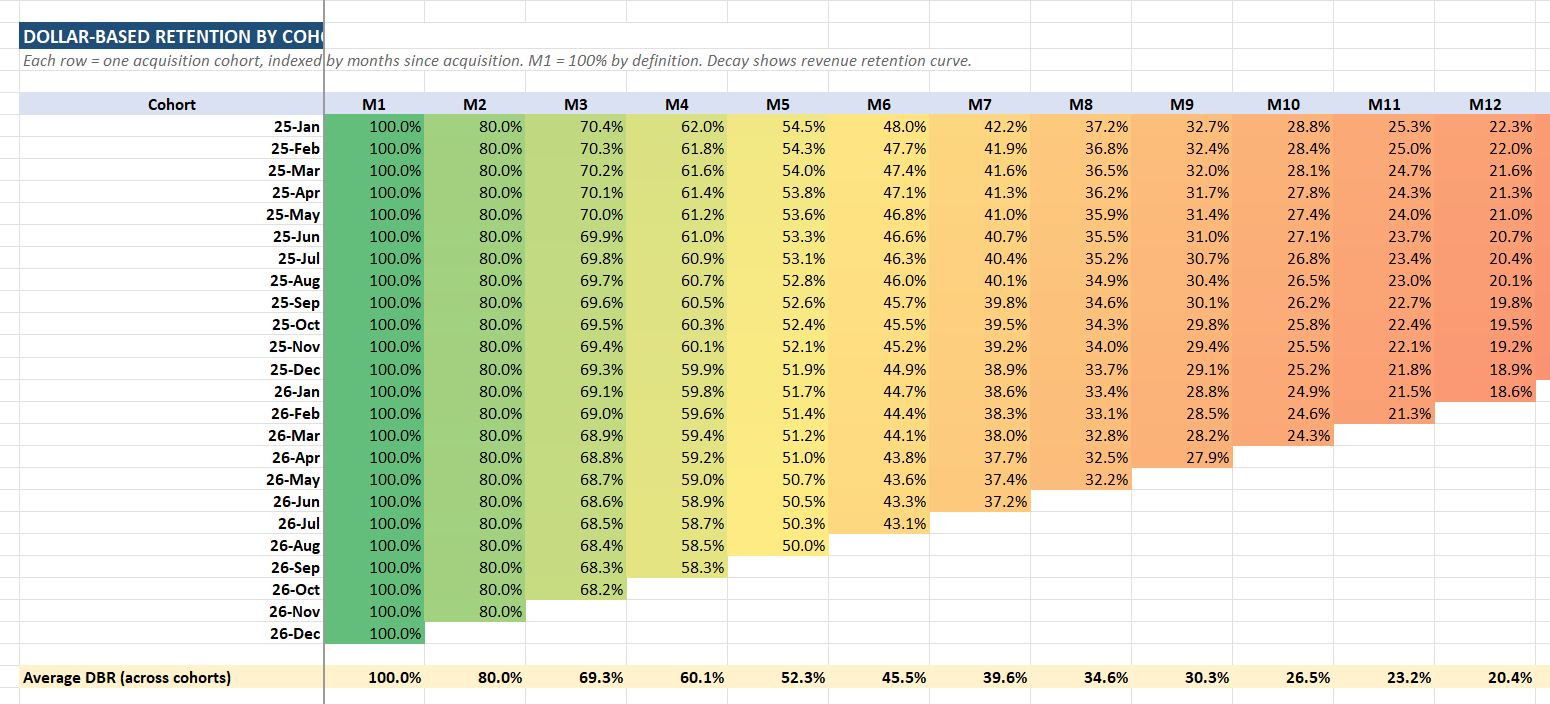

Im probably going to go deeper into reconstructing the cohort model in another newsletter, but its available in my model for what wrok ive done so far. Here is what i get for implied dollar based retention rates. Again I need to go a little bit deeper on all of this. Its also probably changed alot since the 90 day subscriptions came out.

Valuation

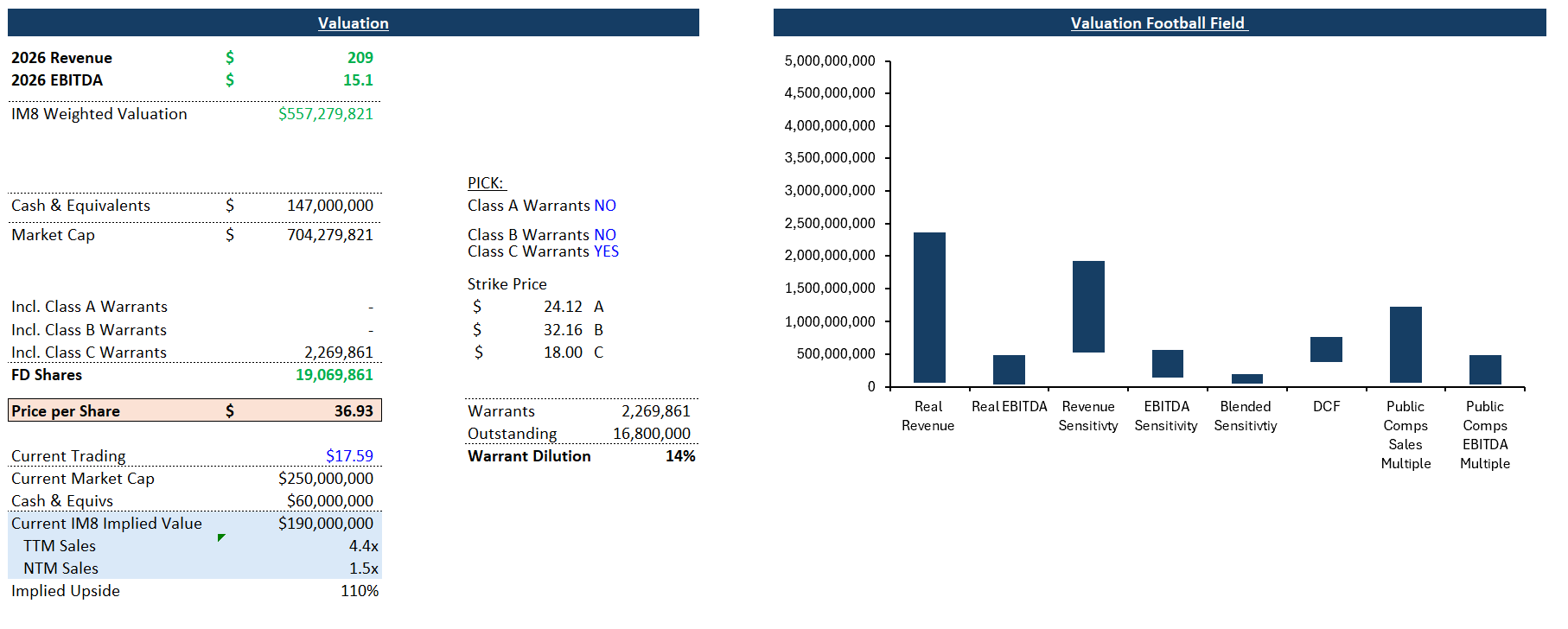

The kicker has always been the valuation. This thing is absurdly cheap. WIth $147m of liquidity and a mkt cap of around 300m, the EV of the fastest growing supplement brand ever sits aroudn 150m. I estimate IM8s intrinsic value is $557m, meaning the market cap should go from 300 to over 700, which would be around $36/share.

This of course is under the assumption they hit their revenue goals, AND become profitable. I think thats the biggest question right now. We really arent given enough info to super clearly underwrite profits.

My updated thinking

I remain highly bullish on PRE as a value growth play. We work with lots of brands that are just like PRE, and I have seen this movie before - very rarely does it stop or even slow down at 14m/mo.

That said, I expect the street will run out of patience before the end of this year if the path to profits does not materialize. If the company were private it would be way more highly valued. In fact, I’m not sure why someone hasn’t tried to take it private at this point. The gross margin progress is a great step in the right direction. Plus, I love the new SKUs, especially the kids as it can extend LTV very meaningfully across households who are already high end consumer spending on im8.

Anyways - stay tuned for an in depth cohort model once i ahve some more time to really dive into it.